India’s aviation sector has become one of the most celebrated symbols of the country’s economic transformation. Passenger traffic continues to expand, airports are emerging across tier-II and tier-III cities, airlines are placing record aircraft orders, and policymakers confidently project India as the future center of global aviation growth. Yet beneath this narrative of expansion lies a fragile reality. The latest surge in Aviation Turbine Fuel (ATF) prices has exposed a structural weakness that threatens the long-term sustainability of the sector. The paradox is striking: the faster Indian aviation grows, the more vulnerable it becomes to fuel shocks. What appears to be an industry soaring into the future is, in many ways, still tethered to unresolved policy distortions of the past.

The current crisis is not merely about expensive jet fuel. It is the outcome of a deeper misalignment between taxation policy, fuel pricing mechanisms, market structure, regulatory design, and airline economics. The Government’s ₹10,000 crore ATF Price Stabilization Fund has undoubtedly provided immediate relief, but it has simultaneously revealed an uncomfortable truth. India continues to treat aviation turbulence through periodic interventions rather than addressing the structural weaknesses that repeatedly generate the turbulence in the first place. The stabilization fund may reduce immediate pain, but it does not eliminate the underlying vulnerabilities.

The numbers illustrate the severity of the challenge. ATF prices recently surged to nearly ₹142 per litre, transforming fuel from a major cost component into the dominant determinant of airline profitability. Traditionally, fuel accounts for around 25–40 percent of airline operating expenditure. Under current conditions, that proportion is approaching 60 percent for several carriers. Such a dramatic increase fundamentally changes the economics of aviation. Every flight becomes more expensive to operate, every route faces profitability pressures, and every airline must rethink network strategies, fleet deployment, and pricing decisions. Growth remains strong, but the financial foundations supporting that growth are becoming increasingly unstable.

The crisis has created a rare situation where both airlines and fuel suppliers find themselves under financial stress. Airlines are trapped in a painful trilemma. They can increase ticket prices and risk weakening passenger demand. They can reduce routes and compromise market share. Or they can cut costs elsewhere, often affecting employment and operational efficiency. None of these choices is sustainable in a fiercely competitive market characterized by thin margins. Simultaneously, oil marketing companies such as Indian Oil, BPCL, and HPCL have reportedly faced significant under-recoveries despite elevated retail prices. This is not a classic case of one side profiting at the expense of another. Instead, financial strain is being transmitted across the entire aviation fuel ecosystem.

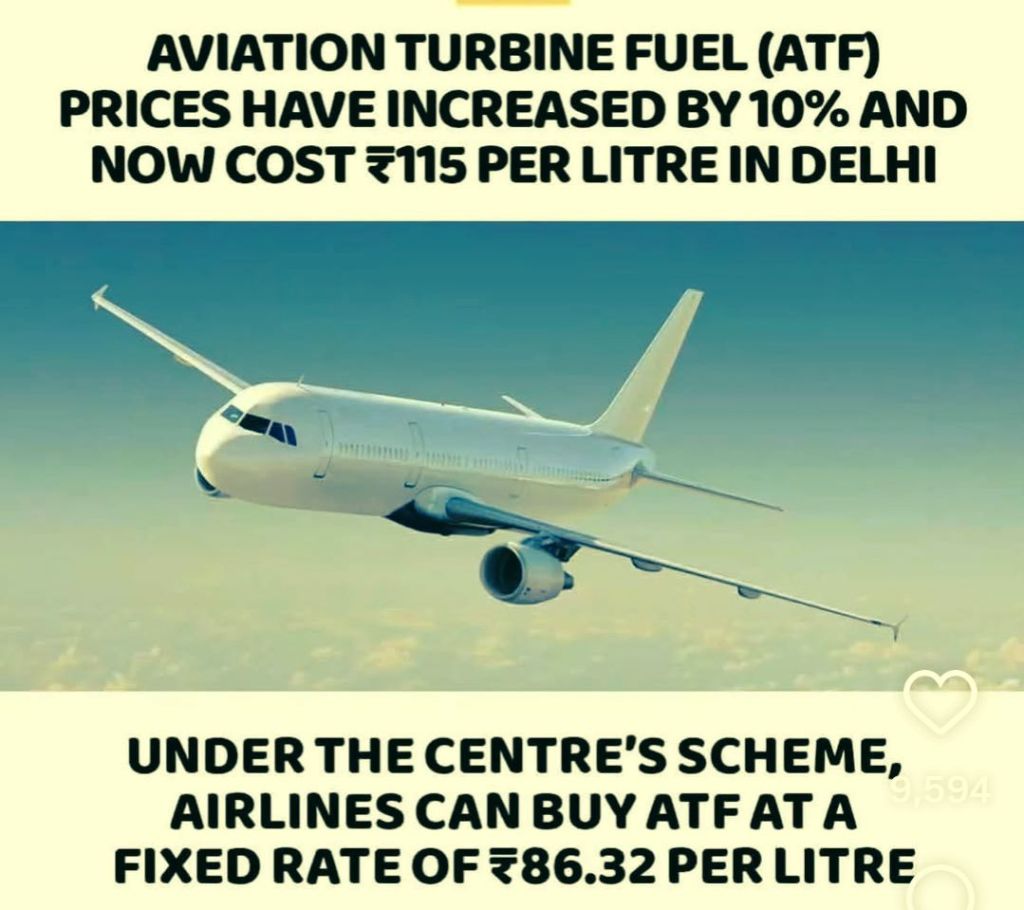

Against this backdrop, the ATF Price Stabilization Fund functions as an economic shock absorber. Structured as an interest-free support mechanism, it compensates oil companies whenever international fuel prices exceed predetermined thresholds. The arrangement effectively caps domestic ATF prices at around ₹86 per litre and international prices at approximately ₹104 per litre. From a crisis-management perspective, the intervention is logical. It prevents sudden fare escalation, protects airline cash flows, and reduces inflationary spill overs. Most importantly, it buys valuable time. However, the very existence of such a fund demonstrates that India’s aviation fuel market remains only partially deregulated despite formal deregulation introduced in 2001.

This creates a peculiar policy contradiction. Officially, fuel prices are market-determined. In practice, whenever prices rise to politically uncomfortable levels, government intervention returns. Such a hybrid model creates uncertainty for all stakeholders. Airlines struggle to design long-term fuel strategies. Investors face policy ambiguity. Oil companies cannot accurately predict pricing mechanisms. Market signals emerge, only to be diluted by administrative action. This uncertainty discourages efficiency and undermines confidence in the long-term policy framework governing the sector.

Even more significant is the fact that lower fuel prices do not automatically translate into lower airfares. Airlines are under no obligation to pass fuel savings directly to passengers. In a market increasingly dominated by two major carriers, competitive pressure to reduce fares remains limited. Consumers may avoid dramatic fare increases, but they are unlikely to enjoy substantial reductions.

Consequently, the stabilization fund serves primarily as a mechanism for industry support rather than direct consumer relief. While this may be necessary under current circumstances, it raises important questions regarding market concentration and competitive dynamics within Indian aviation.

The real structural problem lies elsewhere: taxation. ATF remains outside the Goods and Services Tax framework. As a result, airlines are unable to claim Input Tax Credit on fuel purchases and must instead navigate a fragmented landscape of state-level Value Added Tax regimes. VAT rates vary significantly across states, creating distortions in route planning and inflating operating costs. Bringing ATF under GST would represent the most transformative reform available to the sector. Airlines would gain access to tax credits, improve liquidity, and permanently reduce effective fuel costs. Unlike stabilization funds, which require periodic replenishment, GST integration would create enduring efficiency gains. Yet implementation remains politically challenging because states depend heavily on ATF-related tax revenues. The obstacle is therefore not technical but fiscal and political.

Additional reforms deserve equal attention. Fuel hedging remains significantly underutilized despite its proven effectiveness globally in protecting airlines from price volatility. Direct import of ATF, legally permitted since 2013, continues to face logistical and infrastructure constraints. Expanding storage facilities, improving fuelling infrastructure, and promoting diversified procurement strategies could enhance resilience. These measures may not attract headlines, but they would strengthen the industry’s ability to absorb future shocks without requiring repeated government intervention.

Ultimately, aviation fuel crises are never just about fuel. They are manifestations of broader policy architecture involving taxation, federal fiscal arrangements, infrastructure limitations, market concentration, and regulatory uncertainty. The ₹10,000 crore stabilization fund may help the industry breathe during a period of acute distress, but it resembles an oxygen cylinder rather than a cure. It addresses the emergency without strengthening the patient. Unless India undertakes deeper structural reforms, every future spike in global oil prices will trigger the same cycle of panic, intervention, and temporary relief. The real choice before policymakers is not between high and low fuel prices; it is between perpetual dependence on rescue mechanisms and the creation of a resilient aviation ecosystem capable of navigating turbulence on its own. India’s aviation future will ultimately depend on whether it continues cushioning the landing—or finally redesigns the runway itself.

VISIT ARJASRIKANTH.IN FOR MORE INSIGHTS