India’s Public Sector Enterprises (PSEs) occupy a peculiar space in the nation’s economic imagination. They are not merely corporate entities; they are extensions of the Republic itself—symbols of sovereignty, instruments of strategic control, and often shelters of political convenience. Yet beneath the patriotic language of “public purpose” lies an increasingly uncomfortable contradiction. India’s PSEs today function simultaneously as major fiscal contributors and chronic fiscal burdens. They generate wealth for the state, yet they also drain it. They are celebrated as national assets, yet many operate like institutional liabilities. As India enters the 2025–26 economic landscape with rising expectations and tightening fiscal space, the central question is no longer whether PSEs matter—but whether the country can afford their present design of functioning.

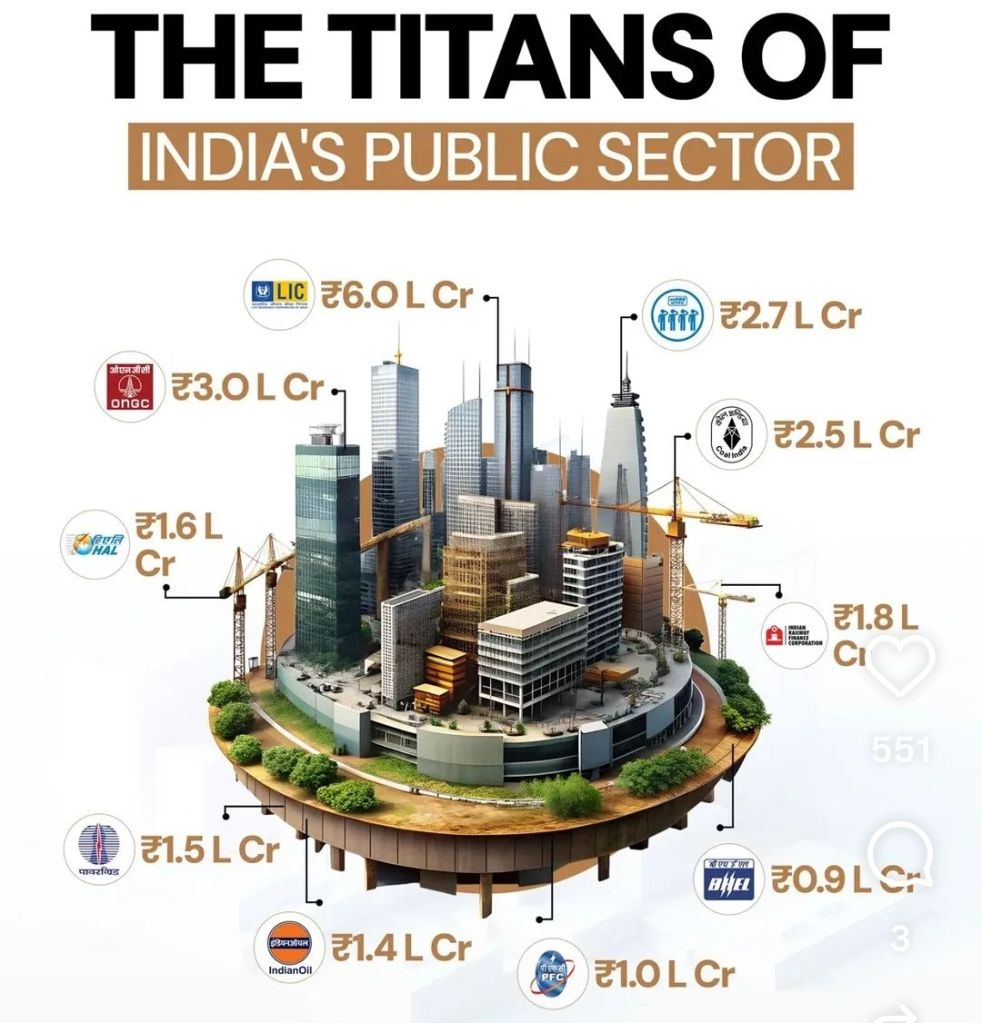

The numbers reveal both the strength and the absurdity of this ecosystem. In FY 2024–25, Central Public Sector Enterprises (CPSEs) contributed nearly ₹4.94 lakh crore to the central exchequer through dividends, taxes, and duties. This is not a symbolic contribution; it is fiscal muscle—equivalent to the budgets of multiple major ministries combined. It also reflects a remarkable increase compared to a decade ago, proving that when managed well, state-owned firms can become powerful engines of national revenue. In an era where every rupee must compete with infrastructure needs, welfare demands, defence expenditure, and debt servicing, CPSEs remain among the few state-owned institutions that actually produce money rather than merely consume it. This alone demolishes the lazy ideological slogan that “public sector is always inefficient.”

Indeed, the more intellectually honest view is that India’s public sector is not a uniform failure but a deeply uneven landscape. Several CPSEs remain globally competitive, operationally sound, and strategically irreplaceable. They built the foundations of India’s industrialisation—petroleum, steel, telecom infrastructure, heavy engineering, and power generation. Even today, they dominate sectors where private capital often hesitates unless offered guarantees, subsidies, or monopoly-like privileges: energy security, defence manufacturing, strategic minerals, and national connectivity.

President Droupadi Murmu’s recent description of CPSEs as “catalysts of growth” is therefore not ceremonial optimism; it reflects an institutional truth. Private capital rarely builds a nation’s base architecture on its own—the state often must build the first scaffolding.

Yet the success of the best CPSEs cannot hide the rot in the long tail, especially at the state level, where inefficiency has become a permanent economic culture. In 2022–23, nearly 490 State PSEs recorded aggregate losses of ₹1.14 lakh crore, and an even more disturbing figure emerged: 308 State PSEs were inactive yet continued receiving budgetary support. This is not governance; it is financial life support disguised as administration. It is the state paying to preserve the illusion of functionality. Nowhere is this dysfunction more visible than in state transport corporations and state power utilities—institutions that do not merely incur losses but institutionalise them. Loss becomes an annual ritual, like a predictable flood: budgets adjust, bailouts arrive, and accountability disappears. The result is a dangerous moral hazard—when failure has no consequence, inefficiency becomes a business model.

The deeper diagnosis is that public ownership is not the disease; governance architecture is. Indian PSEs often fail because the government behaves neither like a responsible shareholder nor like a disciplined regulator. It behaves like a micro-manager, a political sponsor, and a compliance inspector simultaneously. This creates organisational schizophrenia: PSEs are expected to compete like private companies but are controlled like government departments. Political interference remains the most corrosive toxin—commercial decisions like staffing, pricing, expansion, asset monetisation, and vendor selection are routinely contaminated by political calculations. Bureaucratic control compounds this distortion. Civil servants are trained for procedural correctness, not market agility. They naturally prioritise compliance over speed, and file safety over risk-taking. But markets punish hesitation. PSEs, however, operate in a culture where hesitation is rewarded because it reduces the probability of future scrutiny.

This pathology has been further intensified by what may be called audit-driven paralysis. India’s governance ecosystem has created an environment where procurement rules, vigilance approvals, fear of CAG objections, and endless tender protocols often outweigh performance outcomes. Transparency tools such as RTI, digital monitoring, and audit oversight were designed to improve accountability, but they have also produced an unintended behavioural outcome: decision-makers prefer to do nothing rather than take decisions that may later be questioned. The administrative mindset shifts from “creating value” to “avoiding blame.” This is why many PSEs do not fail dramatically—they fail silently, through slow decay, delayed decisions, and missed opportunities. Files move, meetings happen, committees are formed, but competitiveness evaporates.

Equally damaging is India’s absence of a credible exit policy. In private markets, chronically loss-making firms eventually shut down, merge, or restructure. In the public sector, many survive indefinitely because they are politically sensitive, symbolically valuable, or socially inconvenient to close. BSNL remains the most prominent illustration: reportedly loss-making for 17 years, yet sustained due to national security and connectivity logic, receiving bailouts exceeding ₹3.23 lakh crore. This reveals a crucial truth—some PSEs are not commercial enterprises at all; they are policy instruments. But if they are policy instruments, then their losses must be transparently funded as public policy costs, not disguised under the fiction of commercial viability. A state that refuses to admit which enterprises are strategic tools and which are economic failures ends up subsidising both without clarity, and defending both without honesty.

The reform path is therefore not ideological but structural. India does not need blind privatisation, nor blind protectionism. It needs a redesign of ownership and accountability. A Temasek-style model—where government stakes are transferred into a professionally managed holding company or sovereign investment structure—offers a credible blueprint. Such a framework, possibly anchored through a restructured NIIF mechanism, would insulate PSEs from political micromanagement and allow capital allocation based on performance rather than influence. Complementing this, the 16th Finance Commission’s “three-bucket” approach is strategically sound: strategic enterprises must be retained and modernised; potentially viable enterprises must be professionalised and given autonomy; and chronically unviable enterprises must be shut down or privatised without sentimental excuses. A government that cannot close what is irreparably broken is not compassionate—it is fiscally dishonest. India’s PSEs are not doomed by nature; they are damaged by design. If governance is re-engineered, they can evolve from being mythological institutions with balance sheets into what they were always meant to be: state-owned engines of national capability, generating wealth, ensuring sovereignty, and returning performance—not promises—to the taxpayer.

VISIT ARJASRIKANTH.IN FOR MORE INSIGHTS