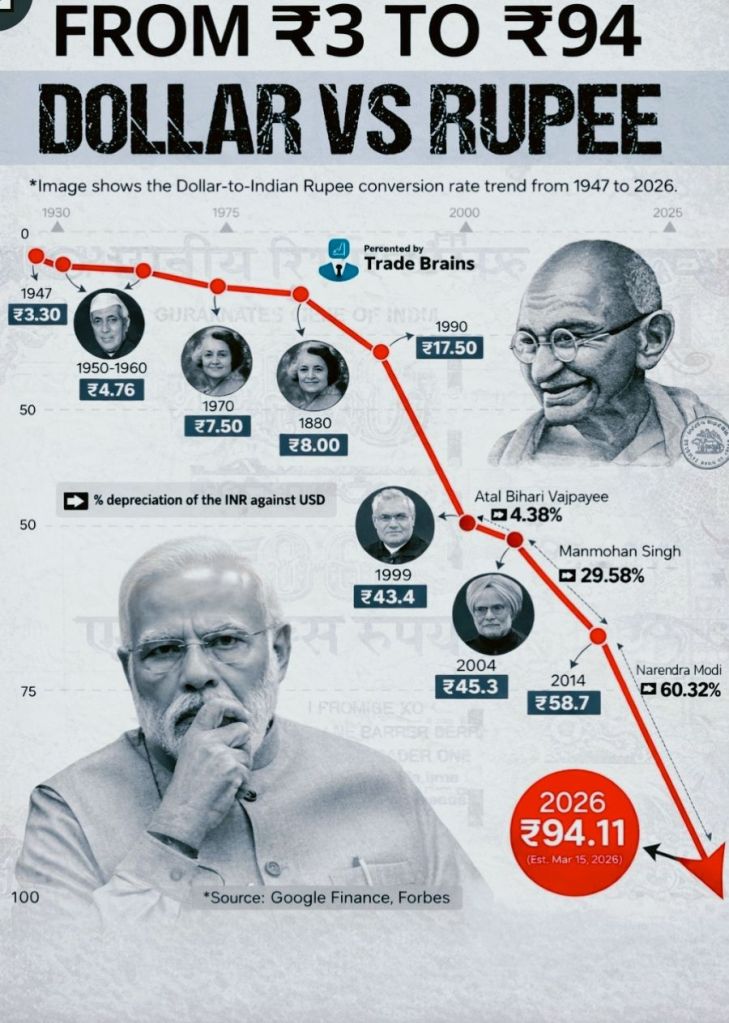

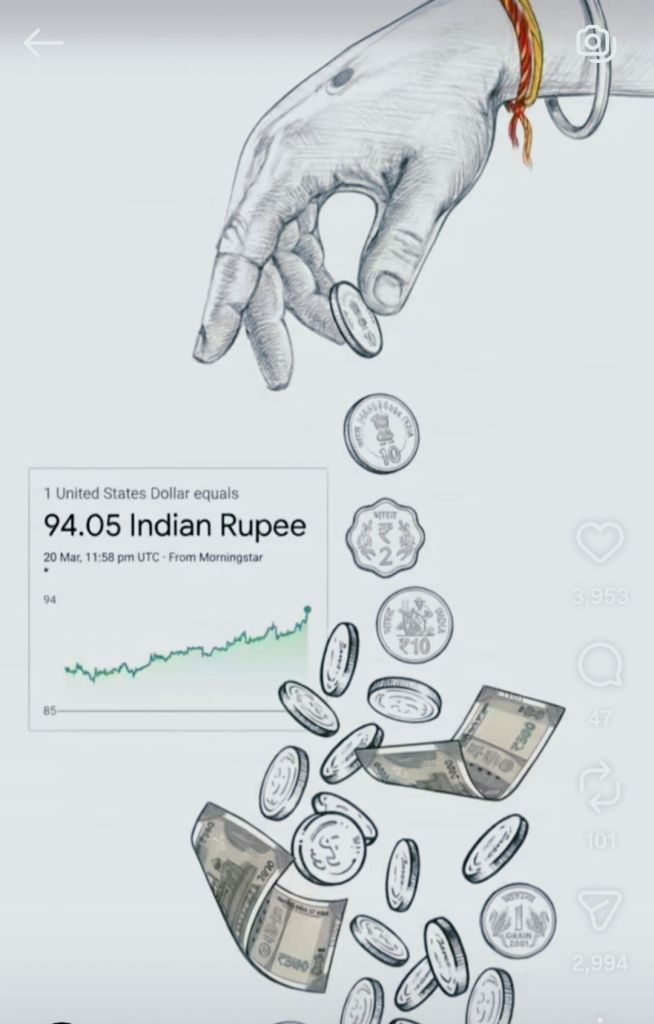

A year ago, paying a child’s overseas university fee or settling a dollar invoice was painful but still predictable. The exchange rate hovered around ₹85.5 per dollar—uncomfortable, yet manageable within a stable band. Today, the dollar trades above ₹94, and the rupee’s decline no longer resembles routine depreciation; it resembles a financial nose-dive. The consequences are immediate and brutally visible: imported electronics turn pricier overnight, medicines with foreign ingredients quietly inflate, and airline tickets rise because aviation fuel is ultimately priced in dollars. The rupee is not merely weakening—it is exporting inflation straight into Indian households, one transaction at a time.

The popular explanation is convenient: blame oil. The Middle East conflict pushed crude above $100, India imports nearly 85% of its crude, and therefore the rupee collapses. This narrative is not wrong, but it is incomplete—and dangerously lazy. The sharper truth is that the rupee was already Asia’s weakest performer even before the war accelerated the fall. While many Asian currencies strengthened against the dollar over the past year, India moved in reverse. The rupee weakened by nearly 10%, making it the worst-performing major Asian currency, and most of the erosion was already underway before the external shock arrived in full force.

The exchange-rate chart tells a story of slow decay followed by a sudden cliff. The rupee began slipping in late February, sliding from ₹85.5 to nearly ₹91 even before the war’s escalation. Then came the vertical drop: conflict acted as an accelerant, pushing the currency beyond ₹94 in under four weeks. This distinction matters because it proves the crisis is not purely oil-driven. Oil explains the speed, but not the direction. The rupee was already wobbling; the war simply kicked the door open and exposed the weakness.

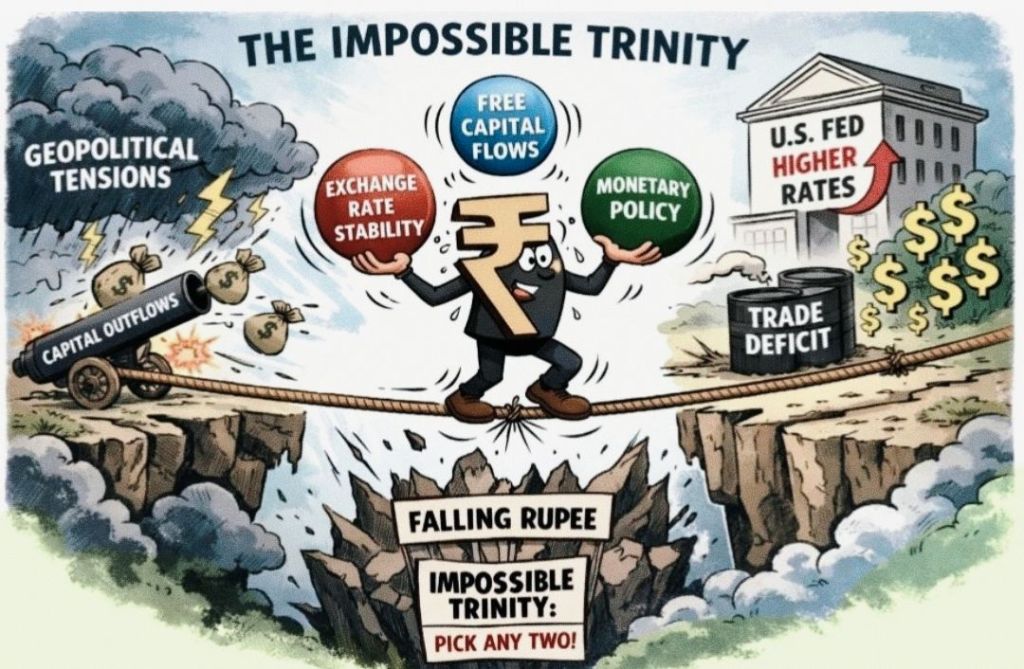

At the heart of the decline lies the simplest equation of foreign exchange markets: India is structurally hungry for dollars. Every time India imports oil, electronics, fertilisers, gold, or machinery, it needs dollars—and to buy dollars, importers must sell rupees. More imports mean more rupee selling, which means the rupee becomes cheaper. The balancing force is foreign capital inflow: when global investors buy Indian stocks or bonds, they must buy rupees, strengthening the currency. But India is currently suffering a double assault—import bills are rising while foreign investors are retreating.

This is where the Reserve Bank of India enters like a firefighter in a city with limited water supply. The RBI can slow panic, but it cannot rewrite fundamentals. Intervention is already visible: foreign exchange reserves fell from $728.5 billion (Feb 27) to $709.8 billion (March 13)—a drop of nearly $19 billion in two weeks, reflecting aggressive dollar-selling to prevent disorderly collapse. But intervention is not a cure; it is a painkiller. The underlying illness remains: India is structurally consuming more dollars than it generates, and markets can smell the imbalance.

Meanwhile, foreign portfolio investors behaved exactly as global finance always behaves during geopolitical turbulence: they fled. In the first 18 days of March alone, investors reportedly pulled out $10.8 billion, compressing a year’s worth of anxiety into three weeks. This outflow is not symbolic—it is a direct strike on rupee demand. When investors exit Indian markets, they sell rupees and buy dollars, intensifying the same dollar shortage already created by oil imports. The result is a self-feeding cycle: weak rupee triggers fear, fear triggers outflows, outflows weaken the rupee further.

Yet the deepest vulnerability is not just crude oil—it is the Middle East’s invisible economic pipeline into India. The first channel is LPG, the gas cylinder in the Indian kitchen, where price shocks immediately become political shocks. The second is LNG, where supply rigidity and Hormuz-linked shipping risks can quietly trigger industrial rationing. The third is fertilisers, where gas disruptions translate into urea inflation, and urea inflation ultimately becomes food inflation—often delayed until the Kharif season. The fourth is remittances, with a major share of Indian overseas workers concentrated in the Gulf; if Gulf economies slow, dollar inflows weaken, and the rupee loses one of its most stable cushions.

This is why estimates like MUFG’s warning—every $10 rise in oil widening India’s current account deficit by 0.4–0.5% of GDP—should not be treated as academic trivia. India’s current account deficit was already around 1.3% of GDP, and with crude above $100, it could drift toward 3%, forcing the exchange rate to adjust downward until the deficit becomes “financeable.” Even the RBI’s REER trend reflects the strain: the rupee’s Real Effective Exchange Rate fell sharply, implying Indian assets and exports are effectively “on sale” to the world. But undervaluation only becomes opportunity if stability returns—and stability is precisely what geopolitics has stolen.

The rupee’s fall is therefore not a temporary currency hiccup. It is a stress test of India’s external resilience, exposing how multiple shocks—oil, gas, fertilisers, remittances, investor sentiment, and widening deficits—are converging at the same time. The rupee is not collapsing because one pipe is leaking. It is collapsing because India’s entire external plumbing system is under pressure, and the cracks were already there before the storm arrived.

VISIT ARJASRIKANTH.IN FOR MORE INSIGHTS

One response to ““The Rupee’s Skydiving Disaster: India’s Wallet in a Dollar Tornado” ”

Good article explaining various reasons for rupee fall. Thank you Sir 🙏

LikeLike