Any serious audit of India’s contemporary economic architecture must begin with a structural reality: a remarkable share of the nation’s critical infrastructure is concentrated within a single corporate constellation—the Adani Group. With a combined market capitalization that has fluctuated in the range of $180–200 billion in recent years, the group occupies commanding positions across ports, airports, power transmission, renewable energy, cement, coal logistics, and urban utilities. Its ascent has mirrored India’s infrastructure acceleration; its balance sheet has expanded alongside the Republic’s development ambitions. To examine the consequences of a hypothetical Adani collapse is therefore not rhetorical theatre—it is a systemic stress test of India’s economic design.

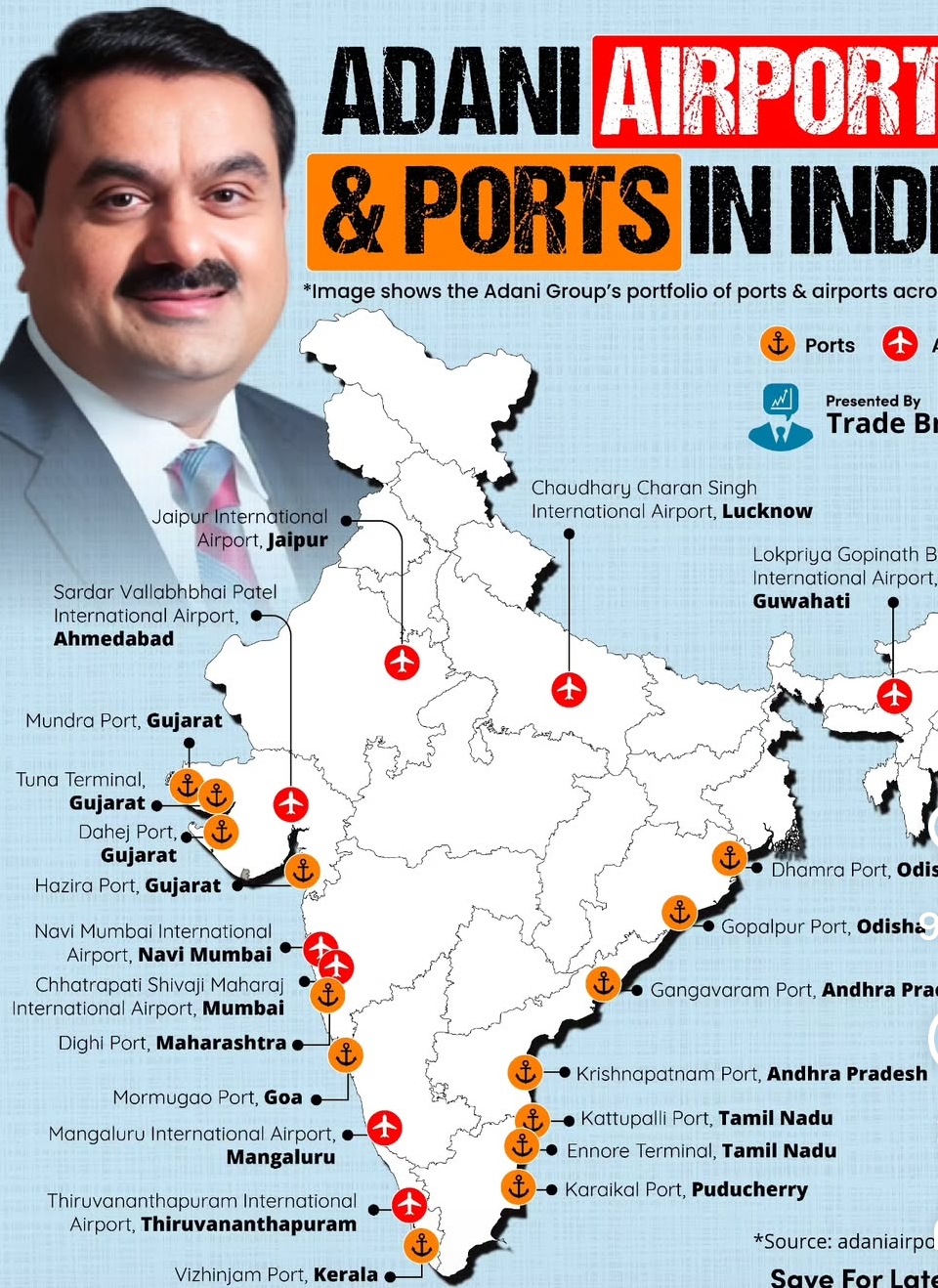

Through Adani Ports and Special Economic Zone, the conglomerate handles roughly 27 percent of India’s port cargo. It operates 15 ports and terminals, including Mundra—the country’s first port to surpass 200 million metric tonnes of cargo in a single year. In a trade-dependent economy where energy imports, containerized exports, and bulk commodities underpin industrial output, such concentration converts operational scale into systemic centrality. A disruption here would not merely dent profits; it would test supply-chain continuity across crude oil, coal, fertilizers, and manufactured goods.

In aviation, the group manages seven major airports, including Mumbai, Ahmedabad, and Lucknow, serving nearly 90–95 million passengers annually. Airports are not isolated assets; they anchor tourism, business mobility, air cargo, and regional growth clusters. Financial distress at scale would reverberate across airlines, hospitality, and ancillary services, with multiplier effects in employment and urban revenues.

Via Adani Energy Solutions and Adani Electricity Mumbai, the group spans thousands of circuit kilometers and supplies India’s financial capital. Its renewable portfolio exceeds 15 gigawatts of installed capacity. Through acquisitions of Ambuja Cements and ACC, it has become the nation’s second-largest cement producer. These are foundational inputs for housing, highways, rail corridors, and urban infrastructure—precisely the sectors driving India’s capital expenditure cycle.

Financial interconnectedness compounds operational weight. Aggregate debt across listed entities runs into several lakh crore rupees, financed by domestic banks, international bonds, and institutional investors. Public lenders, private banks, mutual funds, and the Life Insurance Corporation of India have held varying exposures. The 2023 short-seller episode—when over $100 billion in market value evaporated within weeks—demonstrated how swiftly valuation shocks can propagate into market volatility. Although liquidity stabilized thereafter, the episode underscored equity-market sensitivity to concentrated corporate risk.

In a disorderly default scenario, the first tremor would strike the financial system. Banks would face rising stressed assets; bond spreads would widen; refinancing channels could constrict. Even well-provisioned exposures cannot insulate markets from confidence shocks. Credit tightening would spill beyond infrastructure into MSMEs and consumer lending as risk models recalibrated. Given infrastructure’s role in India’s post-pandemic growth strategy, delays in large projects could depress capital expenditure cycles nationwide.

Capital markets would amplify turbulence. Adani entities feature prominently in benchmark indices; abrupt repricing could erode investor wealth and trigger foreign portfolio outflows. Rupee depreciation pressures might intensify, complicating imported inflation management—particularly in energy and capital goods. Sovereign borrowing costs could edge upward if global markets interpreted the shock as symptomatic of governance fragility. Fiscal arithmetic would tighten through lower corporate tax receipts and potential state interventions to safeguard essential services.

Yet systemic importance does not equate to terminal fragility. Infrastructure assets possess intrinsic economic utility. Ports, airports, transmission lines, and cement plants are productive assets likely to attract strategic buyers, sovereign funds, or creditor consortia under distress. India’s Insolvency and Bankruptcy Code provides a time-bound resolution framework, while regulatory oversight by the Reserve Bank of India and market supervision by the Securities and Exchange Board of India offer macroprudential buffers. The Republic would endure; the question is at what transitional cost.

The deeper vulnerability is concentration. When a single conglomerate spans logistics, energy, aviation, and construction inputs across more than twenty states, systemic relevance becomes structural. Resilience must therefore be engineered deliberately: disciplined leverage, diversified funding sources, transparent disclosures, vigilant lender exposure monitoring, deeper corporate bond markets, and robust competition policy. Competitive pluralism in infrastructure dilutes the “too-connected-to-fail” dilemma.

India’s growth narrative is inseparable from its infrastructure expansion, and the Adani Group has been one of its principal executors. But economic sovereignty cannot rest on the perceived invulnerability of any single corporate empire. It rests on institutional robustness—the capacity of regulators, courts, capital markets, and competing enterprises to absorb shock without paralysis. If an empire were to falter, the decisive variable would not be its fall, but the tensile strength of the Republic’s economic scaffolding.

Visit arjasrikanth.in for more insights